A Heron Data Alternative

Statement Data For Your Books, Not For A Credit Decision

Heron Data is infrastructure for lenders: it parses business bank statements, runs fraud checks, enriches every transaction with categories, and turns the result into underwriting signals like true revenue and NSF days. FlowParse is for the other side of the table — turning financial documents into validated, importable accounting data with native QBO/QFX/OFX/Xero export, self-serve and free to start.

SMB lenders, MCA providers, banks and insurers who need a borrower's statements parsed, fraud-checked and enriched into decision-ready underwriting signals at volume.

Businesses, accountants and product teams who need financial documents turned into validated data their books, returns and accounting software can use.

Why Businesses Look for Heron Data Alternatives

Built for books, not lending

Output is accounting data — signed transactions and importable files, not underwriting signals.

Accounting-ready export

Native .QBO/.QFX/.OFX and Xero/Excel files — the destination a lending platform has no reason to serve.

Balance validation in the box

Opening + transactions = closing, checked arithmetically, with a 0-100 quality score.

Self-serve, no contract

Convert a real statement today — no sales call, no procurement, no minimum.

Invoices and receipts too

The same engine reads invoices and receipts, and reconciles them against statements.

Priced per page

A free monthly allowance and a per-page balance rather than a platform agreement.

Quick Comparison — Heron Data vs ParseFlow

A feature-by-feature look at Heron Data and ParseFlow AI.

| Feature | Heron Data | ParseFlow AI |

|---|---|---|

| PDF bank statement → structured transactions | Yes | Yes |

| Balance reconciliation + quality score | Own checks | Yes |

| Transaction enrichment / categorisation for credit | Yes | No |

| Underwriting signals (revenue, NSF days) | Yes | No |

| Fraud / tampering checks | Yes | No |

| Native .QBO / .QFX / .OFX export | No | Yes |

| Xero / Excel / CSV export | Data via API | Yes |

| Smart Merge — 100 PDFs → 1 Excel | No | Yes |

| Self-serve app for non-developers | No | Yes |

| Free tier, no sales call | No | Yes |

| Invoices and receipts | Business docs incl. insurance | Yes |

| REST API | Yes | Yes |

What Is Heron Data?

Heron Data is built for a specific and demanding job: helping lenders decide. Its customers are SMB lenders, MCA providers, banks and insurers, and their problem is not that a PDF is hard to read — it is that a stack of a borrower's bank statements has to become a defensible credit decision quickly. So Heron accepts PDF statements alongside data pulled from API aggregators, runs fraud and tampering checks on the document, parses the transactions and balances, and then does the part that matters to a lender: enriches each transaction with a category, and aggregates those into the signals underwriting actually uses — true revenue, balance analytics, NSF days.

That is a genuinely different product from a converter, and the numbers Heron publishes reflect the scale it operates at: over 150 customers including FDIC-insured banks and insurance carriers, more than 350,000 documents a week, and around 90% of statements processed without a human in the loop. It also handles business documents beyond statements — insurance policies and loss runs among them — because document-heavy underwriting is the through-line rather than bank statements specifically.

FlowParse sits on the other side of the table. Its users are the businesses, accountants and product teams who need financial documents to become accounting data: [bank statements](/bank-statement-converter), [invoices](/invoice-parser) and [receipts](/receipt-scanner) turned into validated, signed transactions with a [balance check](/features/validation-engine), an [editable review grid](/features/editable-preview), [Smart Merge](/merge-pdf-to-excel) consolidation and native [accounting export](/features/accounting-software-export). We do not enrich for credit, do not score borrowers and do not run fraud checks. Same document, entirely different question being asked of it.

Heron Data strengths

- Purpose-built for SMB underwriting and lending decisions

- Transaction enrichment and cash-flow signals (revenue, NSF days)

- Fraud and tampering checks on submitted documents

- Operates at serious scale for regulated lenders and insurers

Where teams want something different

- Not built for accounting output — no QBO/QFX/OFX or Xero export

- Enterprise sales rather than self-serve, with no free tier to try

- Aimed at lenders reading someone else's statements, not at your own books

- Overkill and mis-aimed if you simply need statements as accounting data

Why Teams Switch to ParseFlow

The right destination

Accounting files your ledger imports, rather than signals a credit model consumes.

Self-serve, today

Convert a real statement with no sales call, no procurement and no minimum.

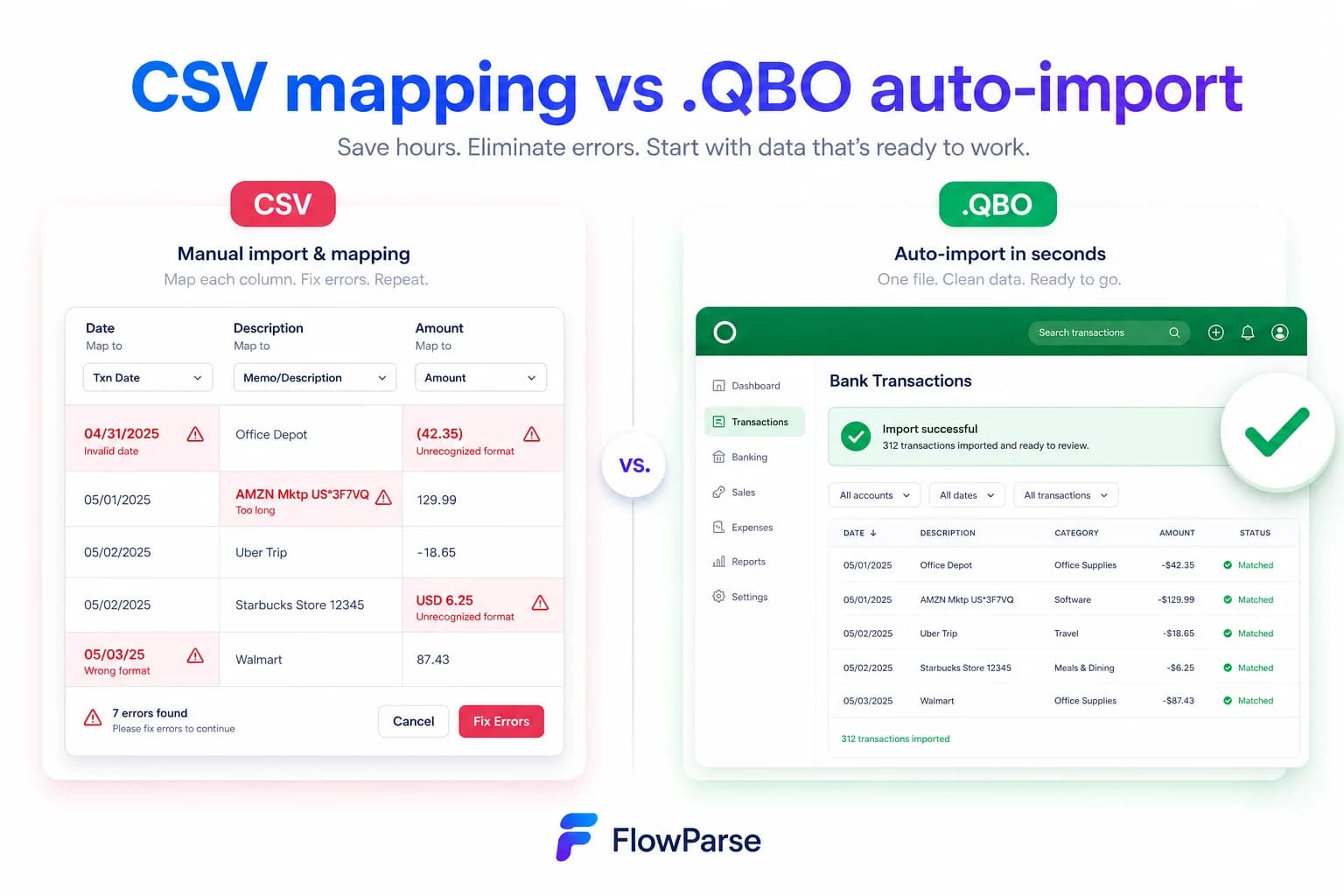

Statements to a real bank feed

Export .QBO/.QFX/.OFX (OFX 1.0.2, FITID de-dup) so imports never double-post.

Consolidate a year at once

Smart Merge combines up to 100 statements into one reconciled Excel.

One engine for the financial set

Statements, invoices and receipts, reconcilable against each other.

Priced per page

A free monthly allowance and no commitment — pay for what you convert.

Underwriting signals vs accounting data

Heron turns a borrower's statements into a credit decision. FlowParse turns financial documents into data your books can use.

Heron path

- Borrower submits statements

- Fraud and tampering checks

- Parse and enrich transactions

- Aggregate into lending signals

- Feed the underwriting decision

FlowParse path

- Upload, or make one API call

- Validated, signed transactions

- Balance check proves completeness

- Smart Merge to consolidate

- Export native QBO/QFX/OFX/Xero/Excel

Pricing Comparison

How the cost and commitment models compare.

| Feature | Heron Data | ParseFlow AI |

|---|---|---|

| Free tier | No (enterprise sales) | Free pages/month + no-signup try |

| Model | Platform agreement | Per page from a balance |

| Buyer | Lenders, banks, insurers | Businesses, accountants, developers |

| Accounting-export files | No | Yes (QBO/QFX/OFX/Xero) |

| Self-serve app | No | Yes (browser app) |

| Setup to first result | Onboarding | None (app) / one call (API) |

Accuracy Comparison

Both platforms use modern AI OCR — here is how extraction quality is assured.

| Feature | Heron Data | ParseFlow AI |

|---|---|---|

| Bank statement transactions | Strong (lending focus) | Every row, balance-validated |

| Completeness proof | Own checks | Arithmetic balance check |

| Transaction enrichment for credit | Yes | No |

| Fraud / tampering detection | Yes | No |

| Debit/credit normalisation | For analysis | Single signed amount |

| Human review step | Exception handling | Editable grid + API |

Who should choose Heron Data?

- SMB lenders and MCA providers underwriting on bank data

- Banks and insurers automating document-heavy submissions

- Teams that need enrichment and fraud checks, not a spreadsheet

- Platforms making credit decisions at volume

Who should choose ParseFlow?

- Businesses and accountants turning statements into books

- Anyone importing into QuickBooks, Quicken or Xero

- Developers who need validated financial data plus export

- Anyone wanting a free, self-serve way to convert a document today

Migrating from Heron Data to ParseFlow

Switching takes minutes — there are no templates to rebuild or models to retrain.

Export your documents

Export invoices and statements from Heron Data or your source.

Upload to ParseFlow

Drag and drop PDFs, scans, or images — no setup.

Review extracted data

Check fields in the editable preview before export.

Export Excel or CSV

Download structured data for your accounting system.

Automate workflows

Use the API and integrations for future documents.

Heron vs FlowParse: the same document, a different question

Comparisons in this category usually turn on who extracts better. This one does not, because Heron and FlowParse are asking a bank statement two different questions.

Heron asks: should we lend to this business? Everything follows from that. The statements arrive from a borrower, so their authenticity is in doubt and fraud checks are mandatory. The transactions matter as evidence of trading health, so each one is enriched with a category and aggregated into signals a credit model can use — true revenue rather than total deposits, NSF days as a distress marker, balance analytics over time. The output is a decision, delivered into a lender's systems, at a volume that justifies a platform.

FlowParse asks: what actually happened in this account, and how do I get it into the books? The statement is your own, so authenticity is not the issue — completeness is. The transactions matter as accounting records, so what they need is a correct sign, a normalised date, a proof that none are missing, and a file the ledger will import. The output is data, delivered to an accountant or an accounting package, priced per page.

Neither is a worse version of the other. If you are underwriting, our validated transactions are a fraction of what you need. If you are closing books, Heron's enrichment is answering a question nobody asked.

Why we do not enrich, and will not pretend to

It would be easy to describe our categorisation as though it were the same thing. It is not, and the difference is worth being precise about.

FlowParse can categorise transactions for bookkeeping — putting spend into the buckets your chart of accounts uses so the year reconciles and the return is right. That is a filing exercise, and being wrong about it means an accountant moves a row. What Heron does is a different discipline: deciding that a deposit is true revenue rather than a transfer or a loan drawdown, spotting the pattern of an NSF, and building the aggregate signals a credit model treats as fact. Being wrong about that means lending money that will not come back.

So we do not claim it. We do not compute revenue quality, do not score cash flow, do not model distress, and do not check whether a PDF has been altered. If your product needs those, building them on top of a converter is a serious undertaking and choosing infrastructure that already has them is the sane move.

The one thing we do that a lending platform has no reason to

Every extraction of a bank statement faces the same silent risk: a row dropped at a page break leaves output that looks flawless. No gap, no error, no low confidence — the missing transaction has no confidence score because it was never seen. In underwriting that risk is managed by scale, sampling and a human-in-the-loop path for the documents the system is unsure about.

FlowParse manages it by making the document prove itself. Opening balance, plus every transaction extracted, must equal the closing balance the bank printed. If it does not, the response says so and names the rows around the break, and the 0-100 score lets a pipeline reject the document automatically. It is the only check that can prove an extraction wrong with no labelled data and no human involved.

That check matters more for books than for lending, which is exactly why the tools differ. A lender aggregating thousands of statements can tolerate noise in one; a bookkeeper reconciling one account cannot tolerate a missing transaction at all, because it is the difference between the accounts tying out and a week of hunting.

The accounting export a lender never needs

Heron has no reason to write a `.QBO` file, and does not. Its data goes to a credit model, and a credit model does not import bank feeds. That is not a gap in Heron — it is the shape of its market.

It is the shape of ours too, in the opposite direction. FlowParse produces real Open Financial Exchange files out of the box: `.QBO` and `.QFX` for QuickBooks and Quicken, `.OFX` for tools like GnuCash and Sage, plus a Xero-ready CSV and clean Excel. Each transaction carries a stable `FITID`, which is what stops a re-import double-posting rows the user already has.

| Layer | Heron Data | FlowParse |

|---|---|---|

| Parse a PDF statement | Yes | Yes |

| Fraud / tampering checks | Yes | No |

| Enrichment + credit signals | Yes | No |

| Balance validation + score | Own checks | Built in |

| .QBO/.QFX/.OFX/Xero files | No | Native |

| Self-serve + free tier | No | Yes |

Bought differently, because sold to different people

Heron is enterprise infrastructure, sold to lenders, banks and insurers — which is entirely appropriate when the buyer is a regulated institution putting a platform at the centre of its credit process. It comes with onboarding, integration and a commercial relationship, because that is what its buyer expects and needs.

FlowParse is a utility. There is no sales call, no procurement and no minimum: a free monthly allowance, no signup required to try it, and a per-page balance after that. See the pricing page; usage is visible per API key, so spend stays predictable and attributable.

That difference tells you almost everything about fit. If your problem justifies a platform, buy the platform. If your problem is a folder of PDFs and a close deadline, a platform is the wrong instrument no matter how good it is.

One engine for statements, invoices and receipts

Where Heron's breadth runs across the documents underwriting touches — statements, insurance policies, loss runs — ours runs across the documents accounting touches. FlowParse extracts bank statements, invoices and receipts with full line items, supplier and buyer details, totals and a tax breakdown, and runs an AI VAT auditor on invoices — all on one pre-trained engine, in a consistent schema.

Because everything comes back in the same shape, an invoice you extracted can be reconciled against the bank payment you extracted from a statement, with no mapping between separate calls. That cross-document reconciliation is the accounting equivalent of enrichment: the step that turns documents into something that answers a question.

A real-world scenario: the tool bought for the wrong job

A pattern worth naming, because the search results that lead here cause it. A finance team at a growing company needs its bank statements as data — several accounts, a couple of years, a migration to new accounting software looming. Someone searches for bank statement parsing, finds a platform built for lenders, and books a demo.

The demo is impressive, because the product is genuinely good. It reads the statements, spots things about the business the team had not noticed, and produces analytics nobody asked for. Then the practical question surfaces: how do we get these transactions into Xero? And the answer is that this was never the point — the platform delivers enriched data into a lender's decisioning systems, not import files into a ledger. There is no `.QBO` at the end of it, because the buyer it was designed for has never wanted one.

The mismatch was set at the search, not the demo. A statement is one document that answers two completely different questions, and the tools that answer them are not interchangeable. If the answer you need ends in your accounting software, the tool should be the one that writes the file it imports — and if the answer you need is whether to lend, no converter will get you there.

Where Heron Data genuinely wins

If you are lending, this is not close. Underwriting on bank data is a hard problem with real money attached, and it needs things we deliberately do not have: enrichment that distinguishes revenue from a transfer, fraud checks on documents submitted by someone with an incentive to alter them, cash-flow signals a credit model can consume, and the throughput to handle a submission queue rather than a folder. Heron reports processing hundreds of thousands of documents weekly for over 150 customers including FDIC-insured banks — that is not a scale you reach by converting PDFs well.

The document breadth is a real advantage in that market too. Underwriting rarely stops at bank statements; there are insurance policies, loss runs and whatever else the submission contains, and a platform that handles the whole submission beats a specialist that handles one document type. FlowParse would be a strange foundation for a lending product — you would be building enrichment, fraud detection and decisioning on top of a tool that has none of them, which is exactly the build Heron exists to save you.

The honest division is by which side of the table you are on. Reading someone else's statements to decide whether to lend? Heron. Reading your own statements to close books, file a return or feed accounting software? FlowParse. The document is the same; almost nothing else is.

A note on who this page is for

Most people comparing these two arrived by searching for something like bank statement parsing and finding both. If that is you, the sorting question is short: is a credit decision involved?

If yes — you are assessing a borrower, an applicant, a merchant — then you want enrichment and fraud checks, and this page has been telling you to look at Heron. If no — the statements are your own or your client's, and the destination is books, a return, or QuickBooks — then enrichment is not the missing piece, and what you want is validated transactions and a file your ledger imports.

Both tools read a bank statement well. Only one of them is aimed at the thing you are trying to do, and the price of getting that backwards is either an underwriting product built on a converter, or a bookkeeping task routed through a lending platform. Neither ends happily.